News

17 July 2023

Global Ports' Q2 and H1 2023 Operational Results

Global Ports Investments PLC ("Global Ports" or the "Company" and, together with its subsidiaries and joint ventures, the "Group") today announces its operational results for Q2 and H1 2023.

Global Ports Investments PLC ("Global Ports" or the "Company" and, together with its subsidiaries and joint ventures, the "Group") today announces its operational results for Q2 and H1 2023.

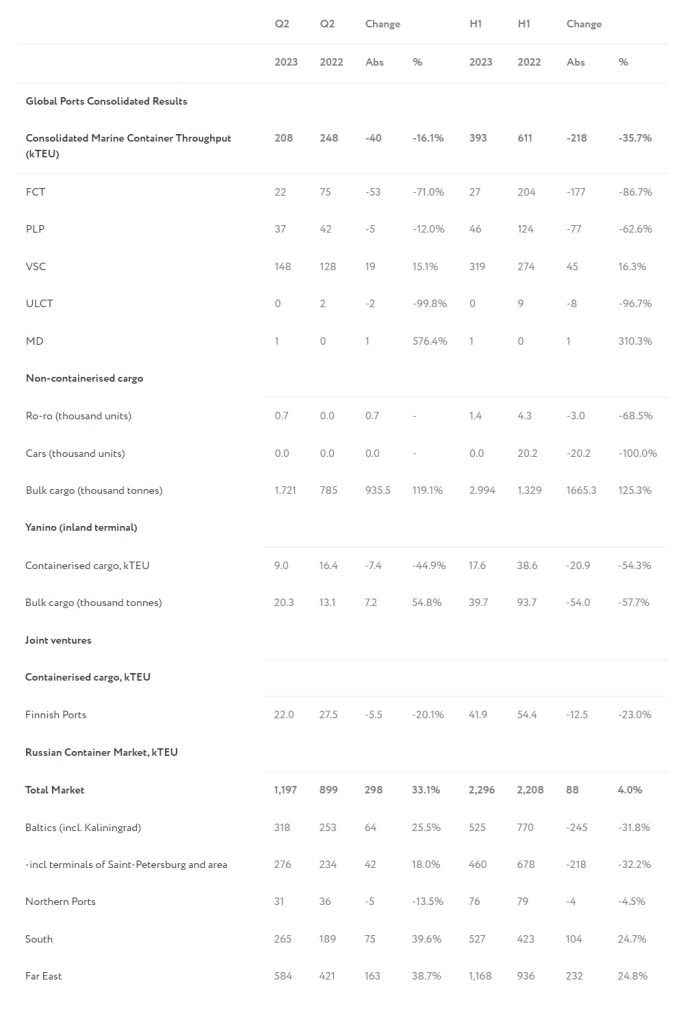

On the back of continuing strong demand in both Far Eastern and Southern basins and gradual increase of direct vessel calls at the Baltics, Russian container market grew in Q2 2023 by 33.1% y-o-y resulting in H1 2023 increase of 4.0% y-o-y.

Marine container throughput at the Group’s VSC terminal in the Far East increased in Q2 2023 and H1 2023 by 15.1% y-o-y and 16.3% y-o-y respectively, while the throughput at the Groups’ terminals in the Baltics declined in Q2 2023 and H1 2023 by 49.7% y-o-y and 78.1% y-o-y respectively.

Overall the Group’s Marine container consolidated throughput amounted to 208 thousand TEU in Q2 2023, an increase of 11.7% q-o-q, compared to the market q-o-q growth of 9.0%.

The Group’s Consolidated Marine Container Throughput declined in Q2 2023 by 16.1% y-o-y as strong performance in the Far East was not sufficient to compensate the decline at the Baltics’ terminals which had been highly exposed to blue chip international shipping lines who left the market in Q2 2022 and Q3 2022. The Group’s Consolidated Marine Container Throughput in H2 2023 declined by 35.7%.

The Group increased its marine bulk throughput in Q2 2023 by 119.1% y-o-y to 1.7 million tons and in H1 2023 by 125.3% to 3.0 million tons as a result of successful efforts to increase utilization rate of temporary available container facilities at the terminals in the Russian Baltics.